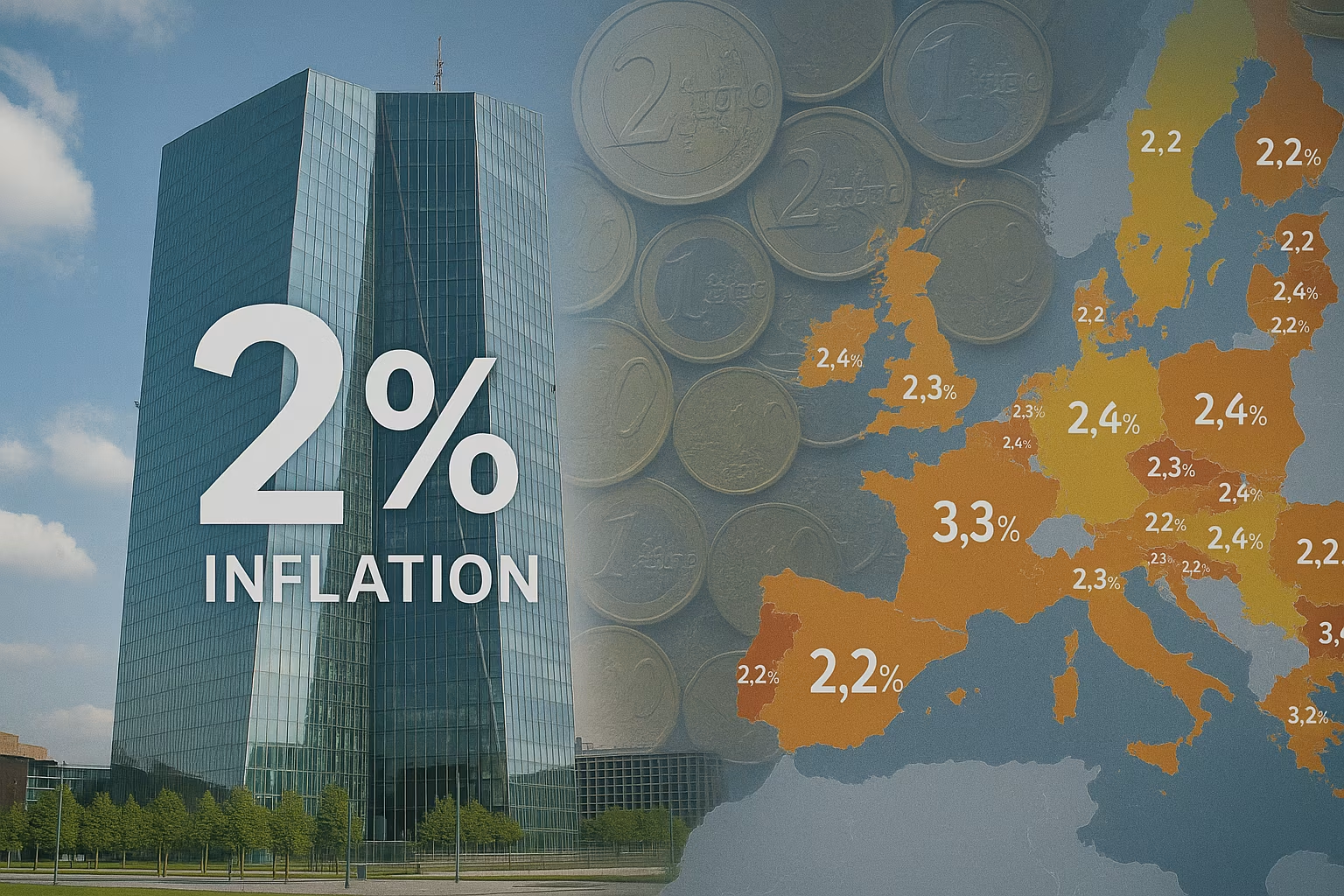

The European Central Bank (ECB) has finally guided euro-zone inflation back to its 2% target—a milestone that many policymakers and market observers see as a victory in its battle against the cost-of-living surge of recent years. However, beneath this seemingly stable headline figure lies a highly uneven inflation landscape across the bloc’s 20 member states.

While the aggregate number paints a picture of price stability, the reality is that countries within the euro area are experiencing markedly different inflation dynamics. These disparities highlight the challenge of applying a one-size-fits-all monetary policy to a diverse economic union.

The ECB’s 2% Goal: Symbolism and Substance

For the ECB, 2% inflation is more than just a number—it’s the cornerstone of its price stability mandate. Achieving this target signals to markets that the central bank has successfully navigated the post-pandemic inflation spike, energy price shocks, and supply chain disruptions that drove inflation to multi-decade highs.

The return to target has eased pressure on policymakers to maintain ultra-tight monetary conditions. It has also calmed fears of a prolonged cost-of-living crisis, offering relief to households and businesses. Yet, the headline achievement masks the fact that some member states remain far from this “sweet spot,” with inflation well above—or even below—2%.

A Spectrum of Inflation Rates Across the Euro Zone

While euro-zone inflation as a whole has landed at 2%, the variation between countries is stark:

- Baltic States: Nations like Latvia and Estonia, which faced some of the highest inflation in 2022 due to energy import dependency, have seen sharper price corrections, with inflation now close to—or even below—the ECB target.

- Southern Europe: Countries such as Spain and Greece are experiencing relatively moderate price growth, helped by declines in energy costs and robust tourism revenue.

- Core Economies: Germany and France remain closer to the average but still face stubborn services inflation, particularly in housing, healthcare, and transportation.

- High-Inflation Outliers: Some Eastern European members within the euro zone are still grappling with elevated inflation due to higher wage growth, persistent food price pressures, and currency-specific factors.

Drivers Behind the Divergence

Several factors explain why inflation rates differ so widely within the euro zone:

- Energy Dependence and Transition

Countries with higher reliance on imported fossil fuels saw sharper price spikes during the energy crisis and are experiencing different speeds of disinflation depending on domestic energy policies and renewable energy adoption. - Labor Market Pressures

Wage growth varies significantly across the bloc. In nations with tight labor markets and strong union presence, rising wages are feeding into service-sector inflation more strongly than in others. - Fiscal Policy and Subsidies

Governments took varied approaches to shielding households and businesses from energy shocks, with some extending subsidies longer than others. The withdrawal of these measures is influencing current inflation readings differently across countries. - Consumption Patterns

Differences in household spending habits—from the share spent on housing to the reliance on imported goods—affect how inflationary pressures are felt locally.

Challenges for ECB Policy

The ECB sets monetary policy for the entire euro area, but it cannot tailor interest rates to the needs of individual countries. This creates a balancing act:

- If rates are kept high to cool inflation in outlier economies, they may unnecessarily slow growth in low-inflation states.

- If rates are lowered to support weaker economies, they could reignite price pressures in countries where inflation remains stubborn.

This tension is at the heart of the ECB’s policy dilemma and reinforces the need for careful communication to manage expectations across the bloc.

Core Inflation vs. Headline Inflation

While the ECB’s headline target has been met, core inflation—which strips out volatile energy and food prices—remains above 2% in many countries. This is particularly true in the services sector, where wage growth and structural cost pressures are slower to adjust.

Policymakers are likely to monitor core inflation closely before making any significant changes to interest rates, as it provides a clearer picture of underlying price dynamics.

Implications for Businesses and Consumers

The uneven inflation picture has tangible consequences:

- Businesses operating across multiple euro-zone countries face varying cost structures, complicating pricing strategies and supply chain planning.

- Consumers in high-inflation regions continue to experience a squeeze on real incomes, even as the euro area average suggests stability.

- Investors must navigate divergent market conditions, with bond yields, equity valuations, and currency sentiment differing across the bloc.

Market Reaction and Monetary Policy Outlook

Financial markets initially welcomed the 2% headline figure, viewing it as a sign that the ECB’s aggressive rate hikes—totaling 450 basis points since mid-2022—are having the desired effect. Euro-area government bond yields dipped slightly, and the euro remained stable against the dollar, reflecting expectations that the ECB may adopt a more cautious stance in future meetings.

However, most analysts agree that any rate cuts are unlikely in the immediate term. The ECB will want confirmation that inflation is sustainably anchored at 2% across the bloc, not just in aggregate.

The Political Dimension

Inflation disparities also carry political implications. Countries still facing high inflation may push for continued tight monetary policy, while those closer to or below target may argue for easing to support growth. This divergence can strain unity within the ECB’s Governing Council and complicate consensus-building on future policy moves.

Lessons From the Inflation Cycle

The recent inflation surge and subsequent cooling have underscored several lessons for the ECB and member states:

- Resilience Planning: Greater energy independence and diversification are crucial for insulating economies from external shocks.

- Labor Market Flexibility: Managing wage growth while protecting living standards is key to avoiding entrenched inflation.

- Fiscal Coordination: Harmonizing crisis-response measures could help reduce inflation disparities in future shocks.

The ECB’s success in bringing euro-zone inflation back to 2% is a milestone worth noting, but it should not obscure the reality of a highly uneven economic landscape beneath the surface. Significant variations in inflation across member states present a continuing challenge for policymakers tasked with steering a single monetary policy for a diverse bloc.

For businesses, consumers, and investors, the headline number offers reassurance—but the real picture is far more complex. As the ECB looks ahead, the focus will shift from celebrating the return to target toward ensuring that price stability is truly shared across all corners of the euro area.